Open Banking is a very real opportunity for innovative New Zealand businesses to further streamline their financial and accounting systems.

Today we’ll look at how far Open Banking has come in the past five years, the potential it holds for a company’s financial systems, and finally, how it would work in practice for businesses using our integrated financial management system, On Account.

What is Open Banking?

Open Banking can be described as a structure and set of standards which give trusted third parties such as financial service providers secure access to banking information through interfaces which connect to bank’s systems.

Put another way, imagine today’s banking customers with their various bank logins as being akin to a house with lights, alarm systems, their garage door, and media systems. These devices all need their own individual controls to be able to operate, just as all banks need their own unique user logins. Open Banking is like switching to a ‘smart home’, where all of these components are now able to be managed with one unified app or login.

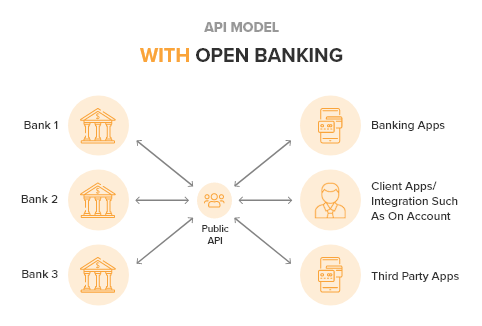

Looking at the back end, the core of the Open Banking structure are public APIs which provide a secure connection to the various banking systems, allowing third party apps to read and create banking data (see image explanation below).

How is the Open Banking API structure different from banking APIs currently in use?

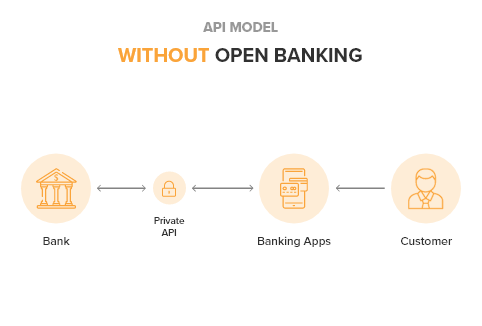

Existing APIs (Application programming Interfaces) are developed and owned by individual banks. An API basically instructs software system components how to interact with each other, it’s the ‘brain’ of a system. These individual banking APIs are proprietary, expensive to build and restricted to use by a single bank’s customers.

By contrast, Open Banking APIs are public. This means developers can ‘tap into’ these public API’s and link their third party apps to a participating bank’s interface. This allows developers to enable connections to multiple banks, integrating the data for personal and business finance apps. From a banking customer’s point of view, it consolidates all their financial data into one app, making it more easily visible and efficient to manage.

What’s good about Open Banking?

Improved access and feasibility. Open Banking means app developers only need to build to a single set of standards, reducing development cost by using one interface that is driven by APIs integrating banking data from different banks. Currently in NZ and Australia, proprietary interfaces are required for every bank.

By virtue of the common set of Open Banking API standards, retail banks can develop API endpoints which can support multiple third party apps, including web and mobile apps, to view account details and pay for goods and services. These collaborative endpoints create efficiency for everyone.

What are the downsides of Open Banking?

As with anything new, there are fears of the unknown when it comes to Open Banking.

A fintech expert, Zafin founder Al Karim Somji says, Open Banking can either be perceived as “a disruptive threat or a competitive opportunity”. Somji notes that data security is the key concern, and acknowledges, “In an industry where data sharing has always been on a risk and permission basis, there will need to be a shift in the security landscape in order for open banking to be successful”.

There are also perceived grey areas around who pays for what, which parties would pay for the needed API development (is it a collective cost or does the biggest stakeholder foot the bill?) and who is liable for any data security breaches should they occur e.g. Would it be the bank, fintech company or even the consumer? This Business Insider article (an excerpt as the full article is paywalled) examines these issues in more depth. For those countries that have rolled out Open Banking, stakeholder payment and security liability varies, and there does not appear to be a one size fits all approach yet.

How is Open Banking already being used in other markets?

In 2018 in the UK, HSBC banking customers started using the “HSBC Connected” app. This app provides a platform for customers to view details of all their accounts, including savings and mortgage accounts, held with 21 participating financial institutions, including Lloyds Bank, Natwest, Barclays and American Express. Although not yet fully developed, the app also lets customers view their spending by category or merchant and forecast balances after future payments have been made. Other Open Banking-enabled services used in the UK include personal financial management tools, credit checking, small business lending and mortgages.

While it’s already live in the UK, US, Europe and Asia, the foundations for Open Banking have only just been laid in NZ.

What is the status of Open Banking in NZ?

Unlike other countries where government regulation underpins standards development, the New Zealand approach is privately driven by the banking industry.

Open Banking protocols and its related payment-related API standards are being developed, maintained and published by the API Centre, a service governed by Payments NZ which is owned by the eight largest banks in New Zealand.

Payments NZ launched The API Centre in May 2019 to provide common payment-related standards on behalf of the NZ banking industry. It manages new and existing standards, and apps developed by Standards Users (API providers and third party API users). The Centre’s website explains their Open Banking journey thus far.

Some API Centre registered third parties have already set up Open Banking based systems like Real Time Debit and Online EFTPOS using the standards. With standards now in place and development projects underway, the industry, government and public will be watching with interest to see how quickly Open Banking systems are adopted in NZ and Australia.

What is the potential for Open Banking for businesses with existing integrated financial systems like On Account?

Several years ago, a major client of ours explored the opportunity of fully integrating and automating payments and transactions with their bank. The total fixed and ongoing bank charges for this project was prohibitive for our client, despite the benefits.

We think Open Banking presents an opportunity for all stakeholders in the banking chain to reduce costs, simplify processes and save time through the integration of relevant apps. Once implemented more widely, On Account clients will soon be able to integrate both enquiry and transaction creation functions. Integration with the public API will become relatively affordable and a standard part of our system. The initial cost and maintenance will be able to be built into the cost of the product and only transaction fees need be negotiated with the bank.

What’s next?

We have been closely watching the developments in Open Banking in Australasia for the last five years, and are excited for this new era of opportunity for our clients as this concept becomes a reality. In December 2019, New Zealand’s Minister of Commerce and Consumer Affairs wrote an open letter to API providers regarding concerns he has about progress in this country’s Open Banking initiatives.

The Minister’s concerns cover the slow rate of progress, differing approaches of API providers which will result in inefficiencies and higher costs of implementation, unwillingness to build to the full scope of the new standards, APIs coming to the market at different times and differences in contractual terms, processes and security standards. All of these factors will slow uptake, add costs and impact consumers.

Australia has addressed this by creating legislative changes including a ‘Consumer Data Right’ which defines rules for consumer data sharing. These rules will underpin the implementation of Open Banking which is still at a relatively early stage. Perhaps similar legislation in NZ will speed the process.

If API providers work together to provide consistency in processes, interfaces, timelines and contractual terms, everyone wins. Data security improvements would be better supported by a consistent and collaborative approach rather than a fragmented one. Consistency and adherence to the complete set of standards would pave the way for wider consumer acceptance and quicker uptake.

If API providers embrace these changes, consumers will have better access and control over their banking data, meaning ultimately more engaged customers.